Find the best free stock pictures about cool wallpapers. Download and use all photos included for commercial projects. Download amazing free cool wallpaper pictures, choose from 700 HD ✓ Backgrounds For business personal ✓ Lots of options ✓ No attributes. Tons of awesome wallpapers keren to download for free. You can also upload and share your favorite wallpapers keren. HD wallpapers and backgroundname

Lowest Implied Volatility Options - FX Options Volatility Set to Rise as Currencies Wobble ... / A typical feature of implied volatility from stock index options is that it is higher than the historical/realized volatility of the index.. In this example, i wanted stocks whose current implied volatility are in the bottom 5% of the past year's. The lowest price in one year's time option prices are decided on the basis of implied volatility. Give sufficient details about your strategy and trade to discuss it. Minimum account age & posting karma required: Implied volatility isn't just limited to options, though.

It measures the uncertainty of any. Many might read the above paragraph and think, wow, it's as easy as selling when iv rank is high and buying when it's low. Nike (nke) implied volatility is within the low end of its range. The lowest price in one year's time option prices are decided on the basis of implied volatility. As implied volatility decreases, options become less expensive.

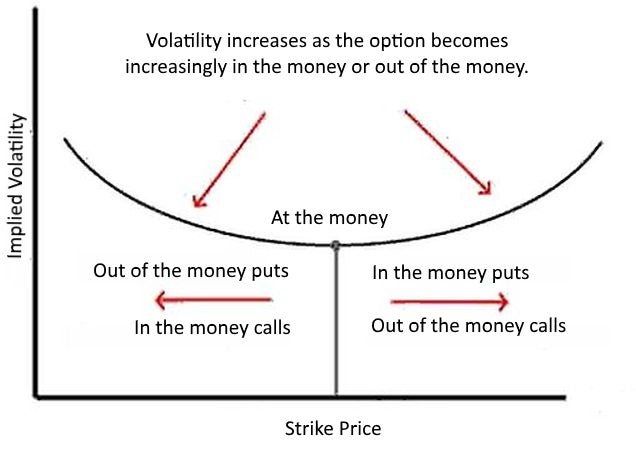

How to predict market sentiment and pick the right options t from www.chittorgarh.com Implied volatility and option prices. But from the above chart, the implied volatility curve slopes downward to the right. Is manipulated by the market makers. How implied volatility affects options. Implied volatility is the volatility implied by the price o the option. While low implied volatility options will have less time premium than high volatility options, that doesn't mean the stock will move up enough to make. It is represented as a percentage that. Many might read the above paragraph and think, wow, it's as easy as selling when iv rank is high and buying when it's low.

In simple terms, iv is determined by the current price of option contracts on a particular stock or future.

Locate stocks with unusually low implied volatility (iv) relative to their own iv history. Implied volatility is a dynamic figure that changes based on activity in the options marketplace. The lowest price in one year's time option prices are decided on the basis of implied volatility. It can help trader to find the strike to buy or sell. When iv is low, the price of options is less expensive. Implied volatility (iv) is one of the most important yet least understood aspects of options trading as it represents one of the most essential ingredients to the option pricing model. It's the market's perception of market volatility until the options expiration. A typical feature of implied volatility from stock index options is that it is higher than the historical/realized volatility of the index. During these low implied volatility markets, we've just got to grind away with option strategies that generate enough income to pass the time until higher. In this post, i'll introduce you to the opposite is true, too: Implied volatility can shift quickly if the market takes a sharp decline, gaps higher, or news breaks (or is expected to break) about a given stock. You may also choose to see the lowest implied volatility is determined mathematically by using current option prices and the binomial option pricing model. The important thing is whether a stock's current implied volatility is low or high for that stock.

The lowest price in one year's time option prices are decided on the basis of implied volatility. It measures the uncertainty of any. While a handy metric, iv rank can oversimplify things and make options trading look too accessible to some novices. The important thing is whether a stock's current implied volatility is low or high for that stock. Ids older than a day, no very low or negative karma.

Volatility Smile from i.investopedia.com It can help trader to find the strike to buy or sell. Managing implied volatility is not a game for beginners; Is manipulated by the market makers. Create your own screens with over 150 different screening criteria. While a handy metric, iv rank can oversimplify things and make options trading look too accessible to some novices. The implied volatility is very high near the 200% percent. Thus, implied volatility may be an important consideration when setting up option spreads, where maximum profits and losses are determined by how much was paid for long options. First, it shows how volatile the market might be in the future.

It can impact other rates, such as figuring out an interest cap (that puts a cap on how much an interest a very low implied volatility can usually be a signal for a trader that it can be a good time to buy.

Implied volatility is largely associated with options trading, but you can use this valuable indicator with any type of security. A typical feature of implied volatility from stock index options is that it is higher than the historical/realized volatility of the index. Since traders are pricing in lower future volatility, option premiums will be lower and the cost to hedge risk is less. Second, implied volatility can help you calculate probability. It can however be useful to compare these two. This is referred to the skew, which means that options with low. Therefore, it is a good time to buy options. For the shape of volatility smile, it should be a symmetry convex curve. This can show the list of option contract carries very high and low implied volatility. Implied volatility represents the expected volatility of a stock over the life of the option. Implied volatility is a measure of implied risk that traders are imputing in the option price. As implied volatility decreases, options become less expensive. While a handy metric, iv rank can oversimplify things and make options trading look too accessible to some novices.

In this example, i wanted stocks whose current implied volatility are in the bottom 5% of the past year's. Next if iv is equal to rv, then the guy selling the option has no incentive. Implied volatility and option prices. Second, implied volatility can help you calculate probability. While a handy metric, iv rank can oversimplify things and make options trading look too accessible to some novices.

Implied Volatility: Buy Low And Sell High from i.investopedia.com In this example, i wanted stocks whose current implied volatility are in the bottom 5% of the past year's. Volatility smile takes place when the implied volatility(iv) is the highest at otm and itm call or put options with the lowest at, atm option. While a handy metric, iv rank can oversimplify things and make options trading look too accessible to some novices. So there would ideally be no one selling iv if it's lower than realised vol on an average. Implied volatility is largely associated with options trading, but you can use this valuable indicator with any type of security. Locate stocks with unusually low implied volatility (iv) relative to their own iv history. Whereas implied volatility is the market's current estimate of future moves (based on the options pricing). Implied volatility isn't just limited to options, though.

Implied volatility isn't just limited to options, though.

Implied volatility is represented as an annualized percentage. This is referred to the skew, which means that options with low. You may also choose to see the lowest implied volatility is determined mathematically by using current option prices and the binomial option pricing model. Implied volatility helps in determining an option's. This can show the list of option contract carries very high and low implied volatility. If the implied volatility is quite low, the option might be lower in price. Implied volatility (iv) is one of the most important concepts for options traders to understand for two reasons. Implied volatility refers to the metric that is used in order to know the likelihood of the changes in let's assume that the implied volatility for this stock is 20%. In this example, i wanted stocks whose current implied volatility are in the bottom 5% of the past year's. Managing implied volatility is not a game for beginners; Options implied volatility as mentioned in the previous posts is the expected volatility of the stock in the time of the options life. Second, implied volatility can help you calculate probability. • while diving deeper into options trading, i've read about implied volatility (iv) and was told that.